It has officially been two months since I started “really” budgeting. Back in August, I wrote a post talking about budgeting and I mentioned a few of the budgeting options that are out there. I mentioned YNAB, Mint, Wallet, EveryDollar, and HoneyFi and at the time of writing the post, I was working my way through the apps and giving each of them a try. Two months later, and I can confidently say that I am extremely happy with one of them, a couple of them are just ok, and a couple I really didn’t like. Off the bat, I didn’t like HoneyFi because you can’t even see what the app does without paying for it. Wallet didn’t have all the funcionality that I wanted, and neither did EveryDollar- too simple for my needs. Mint is retaed as one of the best on the market, and often gets compared to YNAB, but it’s free (unlike YNAB). What I don’t like about Mint is that it is very passive – link your account, transactions will show up, categorize them correctly. For me, Mint is a great way to track spending, but not a great way to actually BUDGET. My favorite of all of them is, hands down, YNAB. YNAB allows you to use the app for 2 months before committing to the paid version and I was 95% sure I wasn’t going to pay for it, but their marketing scheme worked and I as of this morning, I am a subscriber! It’s $84 a year and as they say in their emails, just by budgeting a little, you can “find” $84 and it’s true- I added it to my budget and made room for it. And now I get to track everything and stare at graphs for the next 12 months! How fun! Here I will give you a fulll YNAB review and tell you what I like about it.

Before I start, I will say that if you are interested in trying YNAB, you can use THIS LINK to get 2 months free, and then if you pay for a yearly subscription, you and I will both get an extra month for F R E E. Thanks for your support!

About YNAB:

- YNAB’s philosophy for budgeting your money is that you should be proactive instead of reactive, meaning that you should put your money into “buckets” or categories and you should aim to stay within those limits. If you see that you are overdrawing from one bucket, you can move some money from somewhere and add it to another bucket.

- YNAB allows you to manage multiple budgets with one subscription. For example, I have a personal budget, Luis and I have a shared budget, and I have a Bruja’s Bakery budget. They are under different tabs.

- YNAB allows you to add multiple accounts to the budget and draw money from each of those, or move money within the accounts. For example, Luis has his account, I have a bank account, a cash account, and we have a shared “fun” account. None of these accounts are actually linked to the app- I do it all manually – because this is not an option in Spain, but it would be in the US.

- The unused money from one month will easily rollover to the next month and will appear under “available”.

- When you get paid, the money shows up as “to be budgeted” and you can assign it to categories as you see fit.

- You can create goals. You tell the program that you want to save X amount by X date, and it will tell you how much you need to set aside to make that happen. For example, if I want to invest $6000 by the end of the year, I need to save X amount per month to make that happen. Another example is that Luis and I have a travel bucket which tells us we need to move 150€ per month into that bucket in order to meet our goal. We have been traveling less, but when we do travel, it is pricey and with this bucket, we can see that the money is “available”. I also have a personal emergency bucket, which is really just savings.

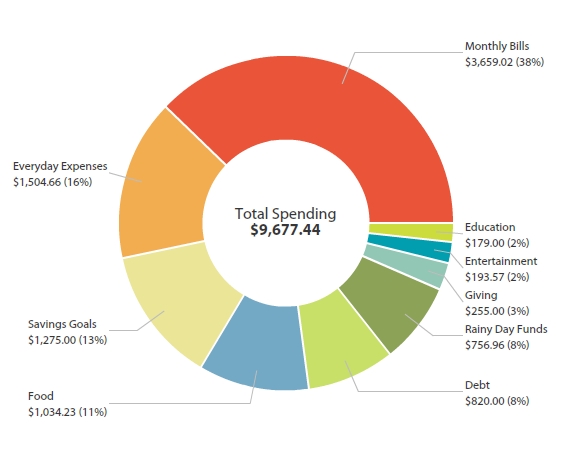

- At the end of each month, you can create various reports and graphs to see where and how money was spent.

What I Like About YNAB- My YNAB Review:

- I like being in control of where my money is going before it goes there. When I want to buy something that I don’t really need, I can see that the money IS available and that I have set it aside for these unneccessary things.

- I like that I can see what we are spending, and where.

- I like that I can pull money from various accounts and move money within those accounts. I use cash often, but card for certain things and I like that everything is separate.

- I like that I can pre-set payments, but they don’t actually go through until I approve them.

- I like that if you overdraw from a “bucket”, it will be red until you move money from another bucket. For example, if we are eating out a lot, I will move some money from our grocery bucket to cover the restaurant budget.

How I use YNAB as a freelancer:

As a freelancer, I don’t have a steady income. Each week varies on how much I will earn and when I will be paid, so what I do is the following:

- I keep an Excel document with all Bruja’s Bakery orders and how much I am earning per week.

- In my planner, I write down all tours and how much I earn per tour and how much in tips.

- On Sunday’s, I “pay myself”, meaning I add my earned income from the last week into various buckets for the upcoming week. I always add a certain percent into savings/emergency and a certain percent into my retirement budget. I add a portion to “fun money” and all 3 of these buckets get topped off each week. Buckets that get money once a month include: healthcare plan, financial manager/advisor, and social security payments, phone, and metro card. Each week, I add a percent of my Bruja’s Bakery earnings to my ingredients bucket, supplies bucket, and taxes bucket.

- I have created a “goal” for my retirement and emergency accounts. YNAB allows you to create a goal, which means that by X month, you will have X saved and it tells you how much you need to put into that bucket per month in order to reach that goal. I use this feature to help me stay on track for these two categories.

How Luis and I Use YNAB Together:

As I said, Luis and I have a shared account that we use for shared things: groceries, restaurants, travel, house things, emergency, eletric, internet, gifts, etc. Each month, a certain amount gets moved from our separate accounts into this shared account, and then in YNAB, I allocate that amount into our joint budget.

- We have a “goal” fund for emergencies, where we keep extra money in case we need it (but really, we can use other money in the case that we REALLY needed it). This is just so we never need to pull from other accounts unless absolutely necessary. For example, once, we missed a flight and had to buy new tickets. This would be a case in which we could use emergency money.

- We have a goal fund for vacation and travel. I know that we don’t travel every month, but when we do travel, we usually spend quite a bit, so it’s nice to know that the money is THERE for when we want to use it- and it’s fun to see it building up!

Takeaway

Overall, I really enjoy the control that YNAB gives me. I have always been someone that likes to know where each of my ducks is and to control where they go, and while I have been writing down every single purchase for the last 4 years, this is the first time that I am actively budgeting my money. I like being able to see that my savings/emergency fund is getting beefed up rather quickly, as is my investment fund, while my “fun money” buckets and other buckets have certain caps. This allows me to say, “I can spend this money how I wish, but when it’s gone, I will need to wait until I refill the bucket”. With Bruja’s Bakery, I like being able to see exactly what I am earning and what is coming out of the account, all in one place. Lastly, I like being able to see that there is money available to do fun things because I know that it’s planned for. I have been on trips where I feel like “I can afford this, but my balance is probably very low….” and now, with YNAB, I can see that my balance won’t change because there is money sitting in the vacation bucket, waiting to be used. There you go, a full review of YNAB.

If you are interested in giving YNAB a try, they offer two months free and if you sign up for those 2 months with THIS LINK and then you later subscribe (pay for the year), you and I will get an extra month free. Who doesn’t like free?! It takes some time to get used to, but once you play around with it, you’ll see how enjoyable it is!